Global Development Workshop-2

March 15, Tuesday, 2022

Prof. Martin Raiser

Thank you, Professor Zha, and thank you, Professor Lin. It's always a pleasure to hear you views Professor Lin, because you have a great ability to present what is a very complex topic in very simple and convincing language. So it would be very easy for me to just say, I mostly agree, but that would be boring for all of you. So I'm going to give you a presentation that raises some questions. Not fundamental questions about the diagnostic that Professor Lin presented, but questions of emphasis.

Ultimately, I will argue that I'm not sure whether industrial policy is that critical, and whether we are helped that much by narrowing the debate about development prospects to one, that whether countries should be allowed to pursue industrial policy or not. Then I'm going to say something at the very end about what I think China could do more for South-South cooperation, given its own success. So I'm going to cover very similar ground that was covered by Professor Lin. But I'm going to take a slightly different approach than his.

So three questions. What can we learn from China's rapid growth about development? Second question, will China escape the middle-income trap? The reason I ask that question is because I want to ask whether the recipe that Professor Lin believes was key to China's success, is likely to be key to China's continuing success going forward, and I'll tell you why I think this is important. Third question, how can China best help other developing countries benefit from its success? So those are my three questions.

What can we learn from China?

The problem that I have here is that virtually every development theory fits China's example quite well. The first development model that we know is the Harrod-Domar growth model, and in which the model development was just driven by investment. China has had lots of investment. And then the second model was by Arthur Lewis, where development is driven by people moving out of agriculture into industry and ultimately into services, and as cities grow, countryside would decline in terms of population. Again, China had lots of urbanization and accelerated industrialization and a large decline in agricultural employment. The next model is by Bob Solo and Trevor Swan, and it was later revised by a few American economists, Greg Mankiw, David Romer and David Weil, and they said that in addition to capital which was key in the Harrod-Domar model of investment-led growth, what we also need to think about is labor, or more specifically about human capital. And this model helps us understand why China grew so fast since 1980.

To see this, let’s look at what kind of country China was in 1980? It was an incredibly poor, surprisingly well-educated country. Or it was an incredibly well-educated but surprisingly poor country. So the point is, China's human capital endowment was very similar to other East Asian economies, but very different to the countries with which it was usually compared, Africa and in South Asia. That made a huge difference for the success of its subsequent growth model, because even though it was low skilled, labor intensive industrialization, most Chinese people could read and write, and most of the countries with which it was compared to had much less human capital. The next set of growth models are those pioneered by Paul Romer and Bob Lucas. They said that these old growth models all assume that growth and development is the result of some exogenous inputs. So you take some inputs and you put them into some production process and out comes economic growth, and they say it's not so easy. They say growth is endogenous and because of this, policies really matter. And I think Professor Lin is a little bit in that tradition, and I think it is the established tradition today. So the points that they make is cities, agglomerations matter. Human capital matters, but also institutions, the degree of competition matters. And clearly in China, policies shifted and this was key to the growth story post-1980.

To sum this all up, in the 2000s, when growth was at the center of what people were thinking about, the World Bank hired a former Nobel Prize Laureate, Michael Spence, to put together a Growth Commission to summarize all this work on growth. I'm not sure this was the period when you were at the Bank, Justin, I think it might have been. The Growth Commission came up with key policies that mattered for sustained economic growth, export orientation, macroeconomic stability, policies to encourage savings, human capital investment, public infrastructure investment, market-based allocation of resources. Finally, we have the new structural economics that Professor Lin is championing and has been arguing very convincingly where growth is driven by industrialization, and industrial policy is key to unlocking industrialization as long as it is consistent with comparative advantage and comes together with public investments to lower trade costs.

So, this is what development theories say. And the Chinese evidence fits all of these theories. So it's very difficult, based on the Chinese evidence, for me to say which of these theories is actually correct. So let me just show you some data to illustrate what I just said.

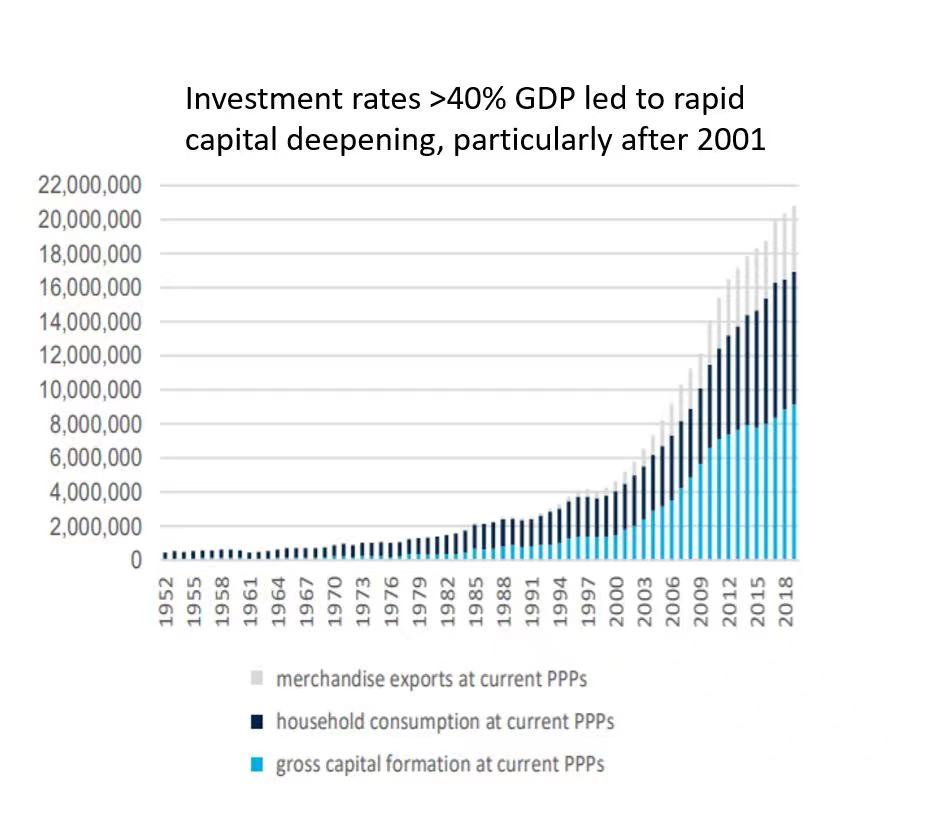

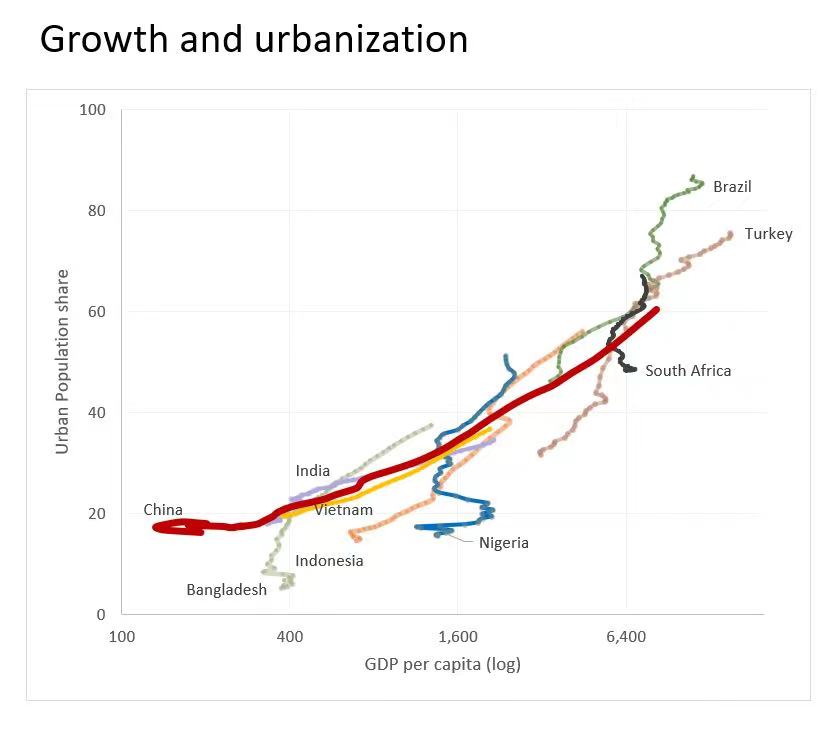

Here you can see investment on the right-hand side, and you can see productivity growth on the left-hand side. And clearly investment played a key role in the China growth story. Here you could see urbanization and the shift out of agriculture. Again, this was really important. By the way, I think Professor Lin agrees with all of this evidence, and his theory is compatible with this evidence too.

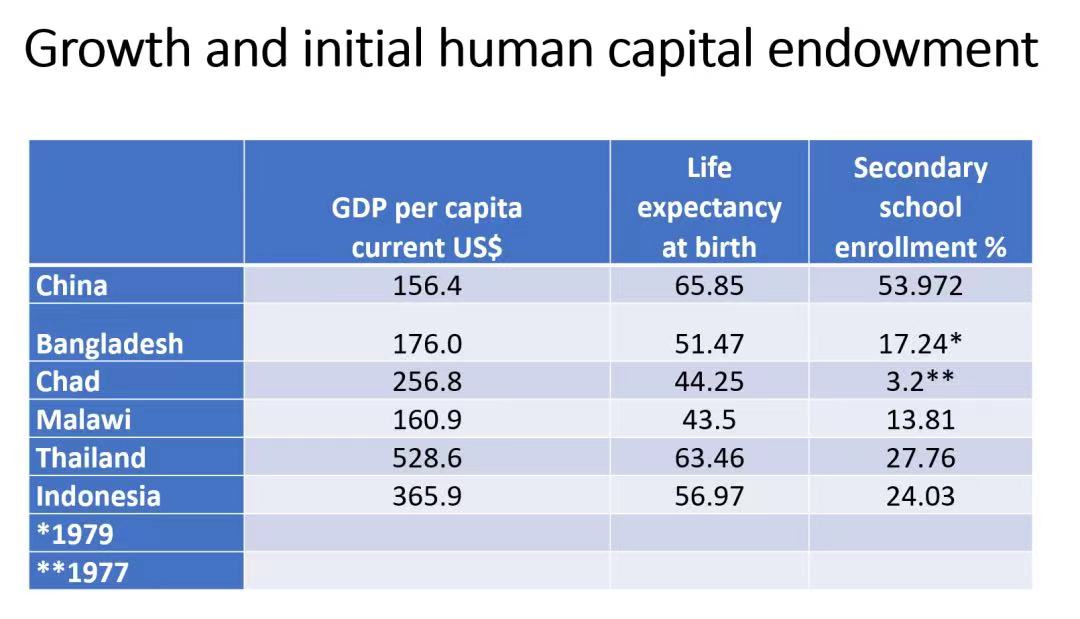

Here is a comparison of China's human capital and its GDP per capita at the beginning of the development process. You can see, compared to Bangladesh, Chard, Malawi, even Thailand and Indonesia, which were considerably richer than China, China's human capital and endowment was significantly higher. So if human capital is critical, maybe the fact that China had quite a bit of human capital at the beginning of its growth process was also quite important.

So, how important was industrial policy? As Professor Lin says, it helped coordinate initial investments by private and public sector investors, and it facilitated imports of critical technology, and crucially, it followed comparative advantage, just like the other East Asian countries had done before. But was industrial policy the critical catalyst? Or was China poised to catch up once it opened its economy? Is there something about the East Asian and China model in terms of putting the role of the state at the center of the development process? Or is it just that East Asia followed an export-oriented strategy, had good macroeconomic policy, was generally favorable to business, didn't have changes in government every two years that fundamentally changed policies, and invested significant public resources into infrastructure? Because if it did all of this, it would be consistent with the advice of the Growth Commission, and we wouldn't need to have a new structural economics theory, because we could just follow the consensus which the Growth Commission established.

So I think what Professor Lin wants to argue about is that we do need a new structural economics theory, because the reason a lot of other countries fail in their development aspirations is that just following the Growth Commission is not enough. You need the state to take a more active role, otherwise it just doesn't come together. This is the magic sauce. This is the critical ingredient that is missing in the development strategy of a lot of other countries. And my contention is that I don't think this is the critical sauce. My view of industrial policy is that it doesn't do any harm if it is added to all the other ingredients that are already in the sauce. In fact, it may well do a lot of good. But the first thing that countries should do if they want to know whether they have a good chance of development or not, is to look at the ingredients that the Growth Commission identified, as critical as having a good broth, and then add the magic sauce if you want, but if you are missing the other ingredients, the magic sauce may not do that much for you.

Now, if this ingredient, the leading role of the state, is so important, then surely this should be a key ingredient also for China’s growth going forward. And that's the reason why I'm asking the second question about whether China can escape the middle-income trap. And I'm going to look at a number of factors that are aligned with traditional development theories, and I'm not going to look at industrial policy. I think I can argue that these other ingredients are the more difficult challenge for China to overcome than the need to reinvent its industrial policy. That doesn't mean that the industrial policy may not be critical to China going forward, but it does mean that the other ingredients may well be the more binding constraints. And by implication, I think that may also be true, or may have been true, for China's development up to now. So the short answer to the question “Will China escape the middle income trap?” is yes. But the next 40 years will be tougher than the first and the government may need to focus more on the binding constraints than on a new industrial policy.

The first thing that China will confront is that its human capital advantage at the beginning of the transition has turned into a human capital disadvantage compared to countries that were upper middle-income countries 20 years ago. So Professor Lin uses, I think, a very nice heuristic, where he says, look, if you want to be Germany at the end of your development process, don't look at what Germany does today. Look at what Germany did around the time when it was where you were today. Or similarly, for China, if you want to follow the track of Korea or Japan, although Japan has been slightly less successful, or even Singapore, then look at where any of these countries were when they were around $12000 per capita? And the point about human capital in China is to argue that at $12000 per capita, all of these other countries had much higher levels of human capital than China does today. So compared to very poor countries, China was well endowed with human capital, but its economic growth has been so rapid that the amount of investment in human capital, in deepening the level of education and an upgrading the skills of the workforce, has not been sufficient for China to keep pace with the speed of its economic development.

In 1990, the average rate year of schooling of the working population in Korea was several years longer than the average rate of schooling of the Chinese working population today. So human capital will be a constraint. Of course, China is investing a lot in expanding TVET and expanding other forms of education, so it may well catch up on that handicap, and there may even be a growth impetus coming from this. But I believe that this is a risk to China's future growth and prosperity. Aging is another demographic factor which may militate against China's economic prospects going forward. Japan is a very good example.

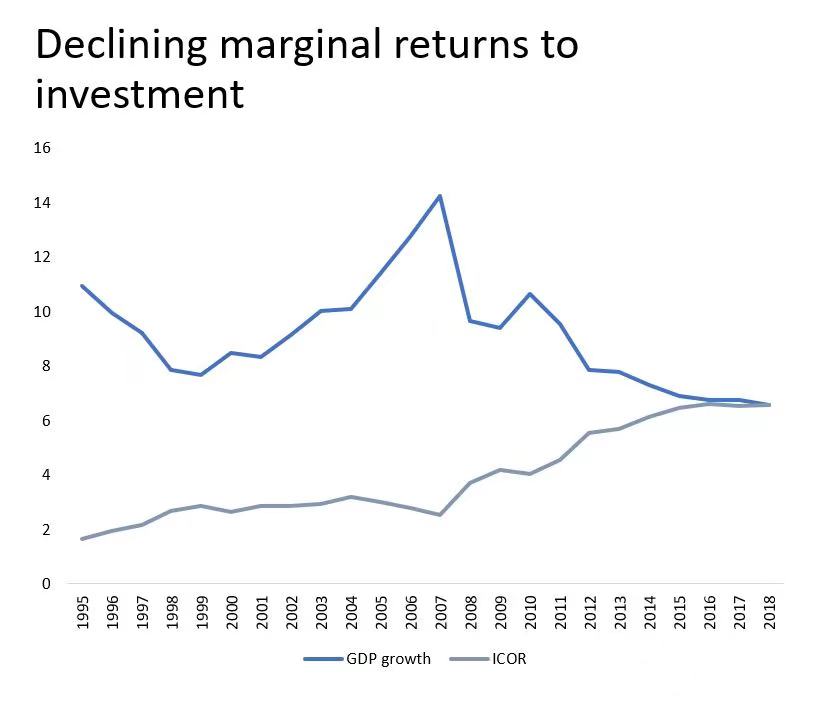

China belongs to a group of countries that grew very fast because they invested a lot in physical capital. But all of these countries, from Japan to the former Soviet Union to other parts of East Asia, ran into the problem that after a while, there is only so much physical capital that you can invest in. And the most productivity enhancing modern investments require much less physical capital than the traditional technologies. They're much more driven by latent capital, by knowledge capital, by talent, etc. So just putting in more money, putting in more investment, doesn't give you the same return as it did in the past. So you have declining productivity growth, as a result of declining returns to investment, but also the declining economic dynamism. I talked about the role of competition, and we see some evidence of, although not very conclusive, decreasing pressures of competition.

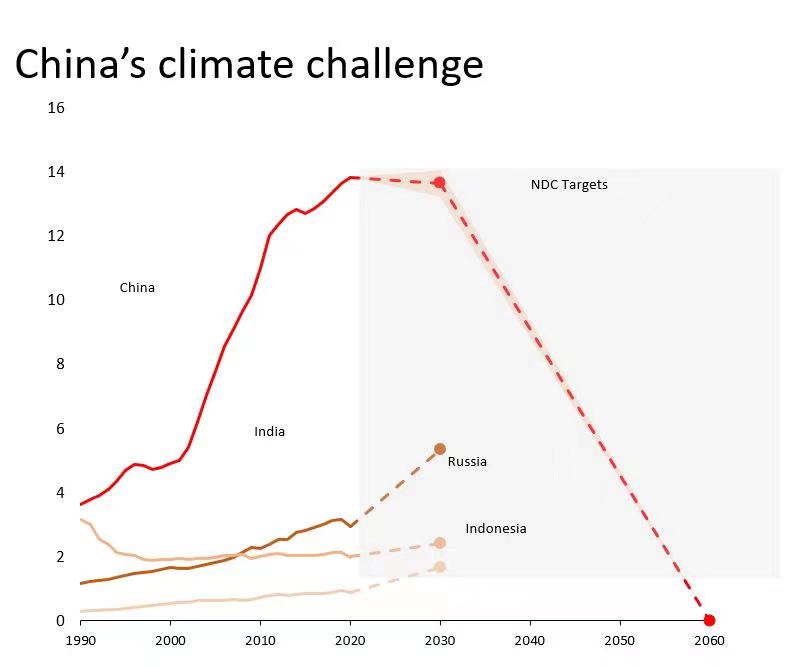

And then finally, something that doesn't appear in any of the traditional growth theories, which is the challenge of the climate transition. So yes, industrialization is a great driver of economic progress, but in an age where we're trying to get rid of carbon, industrial dependence is also a challenge, because industries consumes a lot more energy, industries produce a lot more carbon. So for China to sustain its growth, it needs to find a way either to move out of industry or to decarbonize industry. Both of these are going to be challenging. They also present opportunities, but they could be challenging.

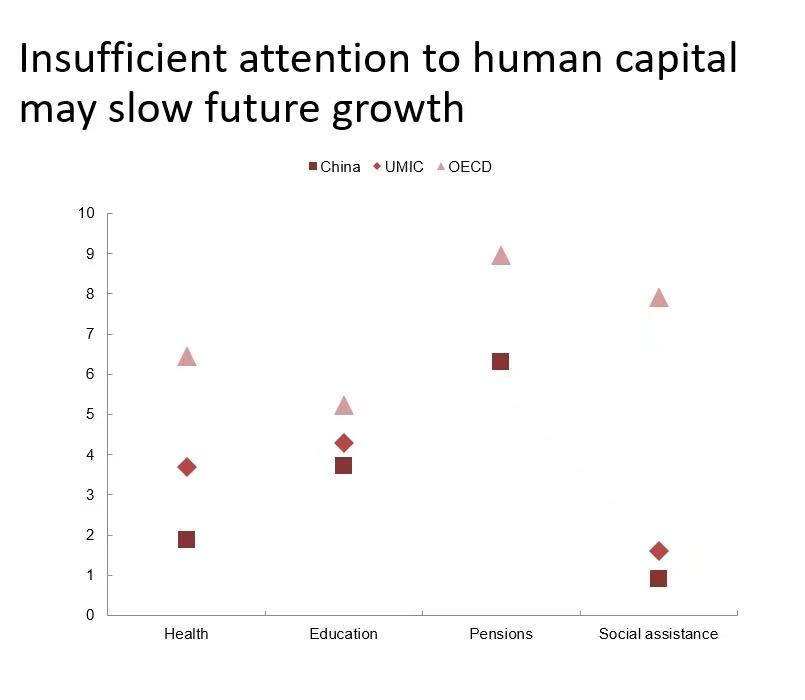

Again, some data on the issue of declining returns on investment. On the left, you can see how growth declined, and the inverse of the investment rate, the amount of investment that you have to put in to get an additional amount of output has gone up. On the right-hand side, insufficient attention to human capital. You can see how China, compared to other upper middle-income countries, and also the OECD countries, invests a lot less in health, significantly less in education, and has much lower levels of welfare spending more generally.

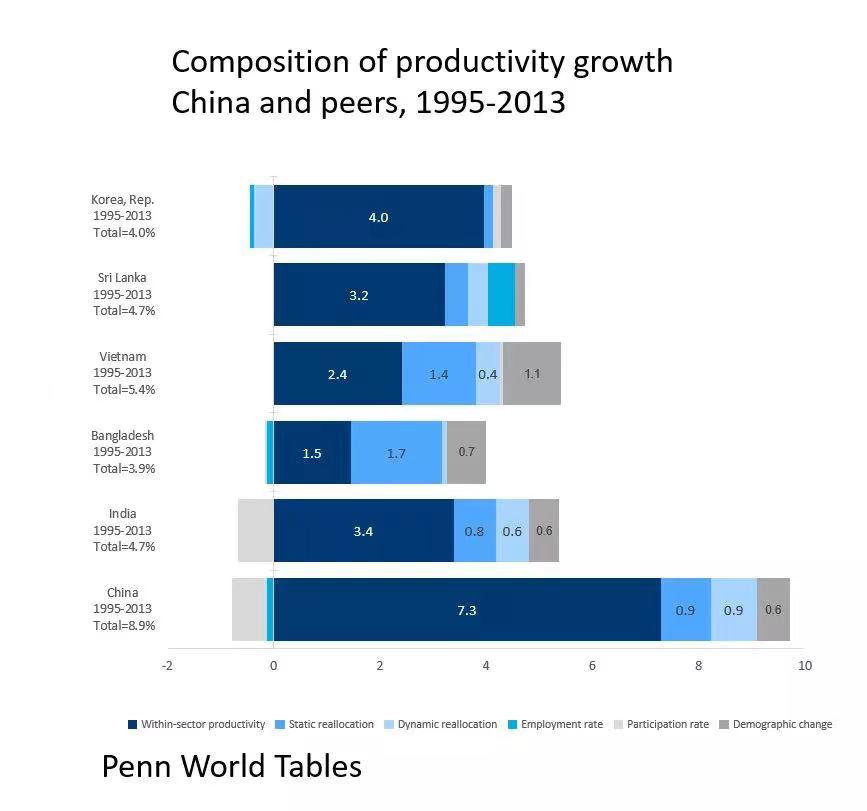

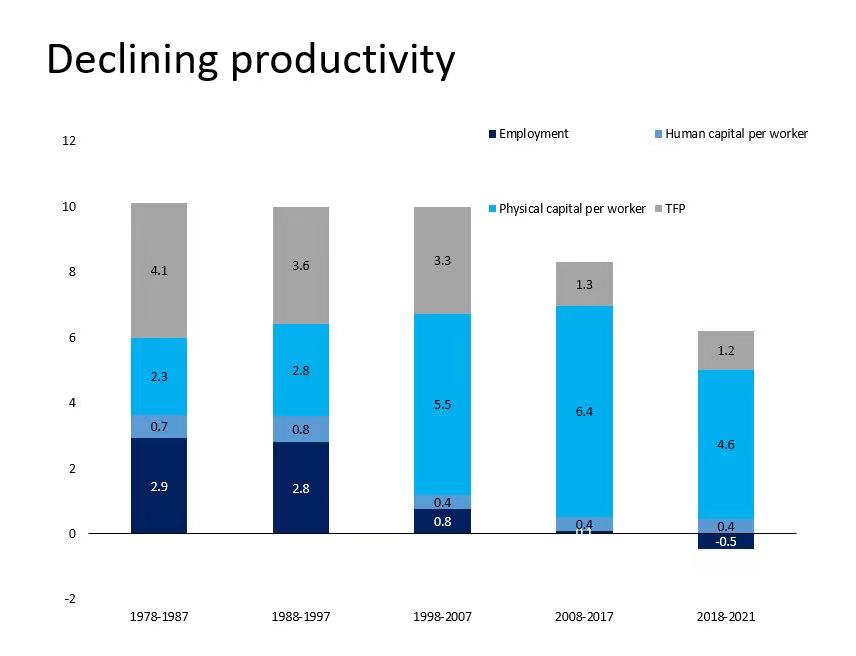

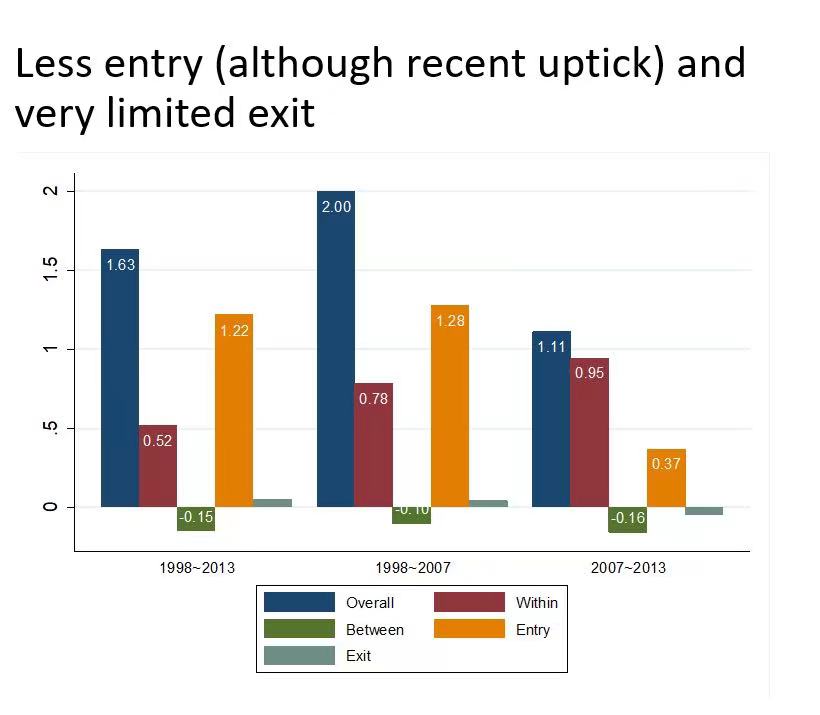

Declining productivity and reduced business dynamics: On the left, you could see how growth in China originally was essentially based on equal measure of employment growth, physical capital growth, human capital growth, and quite a lot of total factor productivity growth, and how the role of total factor productivity growth has declined and that of physical capital increases, and the previous slide showed you why that may not be sustainable. There has also been less business entry and very little exit, at least in the data up to 2013. I think the recent data show a slightly different pattern, so maybe this is less of a constraint.

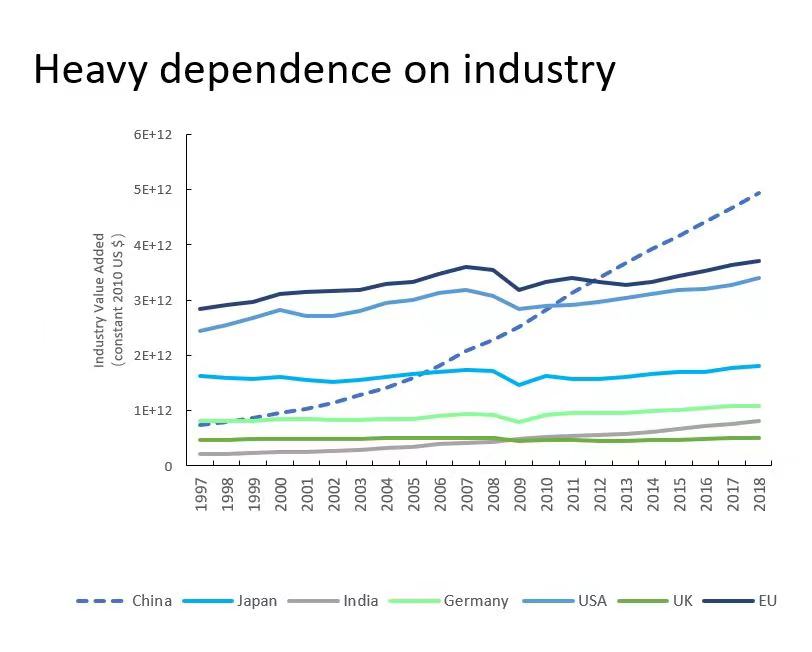

Then finally, very heavy dependence on industry, and the climate challenge that China will have to confront. Again I think China will do it, because China is very successful at adapting its economy. But I'm not sure the solution to any of the problems that I just mentioned is industrial policy. Maybe in the case of the climate challenge, industrial policy has an important role to play, but in all of the other cases, I would argue other constraints that are more in line with traditional growth theories are at least as binding as the presence of a strong state to coordinate economic activities.

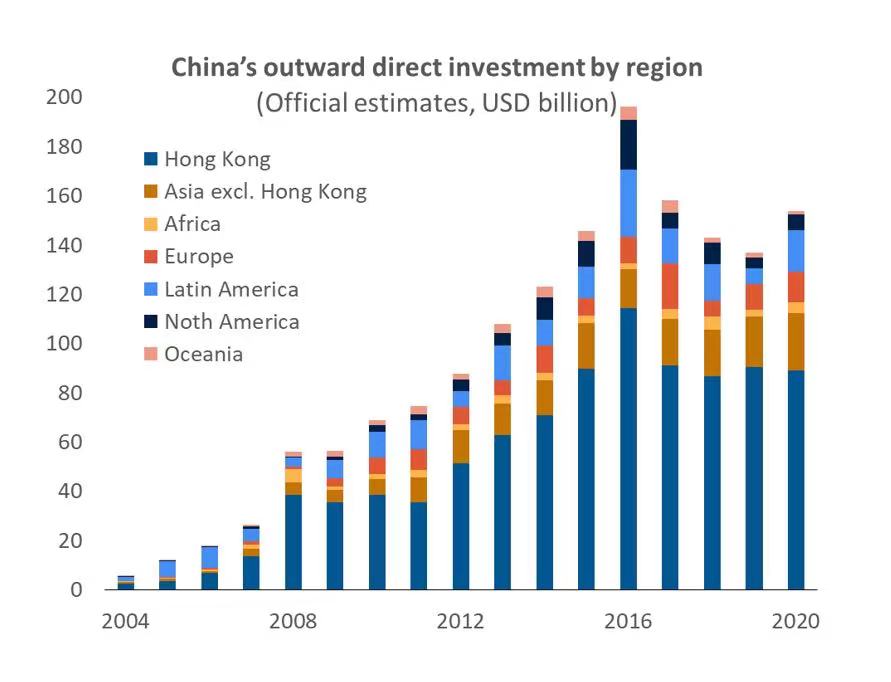

Now let me turn to the 3rd question: How can China benefit other developing countries? A lot of attention has been placed on China's investments abroad, and overall, I would argue those are a good thing. But I do have to say, because we have worked quite a bit on this, that China’s overseas investments, unfortunately, are characterized by some beginner mistakes, taking a lot of risks and using poor mitigation strategies. And going forward, to get more out of Chinas investments abroad, it would need to address some of those shortcomings. But because I spoke longer than I intended, I'm not going to go through the remainder of my slides. I'm just going to dwell on the last two points on this slide, and emphasize those because I think they resonate very well with what Professor Lin said at the end of his presentation.

There are two areas which, in my view, deserve much more attention than the discussion about China's investment strategies abroad, and whether it did good or bad in investing capital. Again, as I said, I think the world needs sources of investment. Western sources of investment were retrenching. China came in. I think China needs to learn to do it better. But overall, I would much rather have China investing than China not investing. There's no question in my mind about that.

Topics to explore futher

But two areas didn't receive a lot of attention. First, a lot of what China can bring in benefit to other countries, and Professor Lin is a key example of this, is to tell China's story and to share China's experience. And yet, China does not tell its story very well. I wish there were more like Professor Lin who does it so well, as he did tonight. But when you look at the difficulties that we in the World Bank have to tell China story, you may see what I mean. China is the world's biggest poverty reduction story, yet the number of people who have access to the data which enables one to analyze the key drivers of that poverty reduction was is a handful of people. Even within the Chinese government, people don't get access to those data. Similarly, China has some of the best performing schools in the OECD ranking on PISA, there is a lot of interesting analysis of the Shanghai model of how did Shanghai become so successful in education rankings, and yet, for the rest of the country, we have very little data. So we are meant to generalize from the Shanghai example, which is not representative to the example of China as a whole. A lot of experience that China has for developing countries would be much more relevant if you go to places like Yunnan or Gansu or some of the interior provinces. Yet data on the educational performance of those schools is not easily available for analysis. So those are just two examples. There are others, data on fiscal performance, on returns to government investment. There's a lot of analysis being done, and a lot of good academic analysis being done, but given how important that China model is, it would be great if we had better access to Chinese information.

And the second point is that where China, I think, is underplaying its hand and could be making a larger contribution, is in the role of its domestic market. China's domestic market, its domestic final consumption, is worth roughly $6 trillion. By comparison, the US is, I think, roughly twice that size, and Europe is around to $8-9 trillion. So the US consumer market and the European consumer market are still larger domestic markets than China. But if China were to increase the level of final consumption closer to what it is in OECD economies, let’s say even just to the bottom of the distribution of the OECD, not to the middle, then it would increase the share of final consumption in GDP by around 10 percentage points. Because China invests so much, it consumes very little. And if it did increase the share of consumption in GDP, and taking into account China's continued economic growth, then the size of China's final consumption market could double over the next ten years.

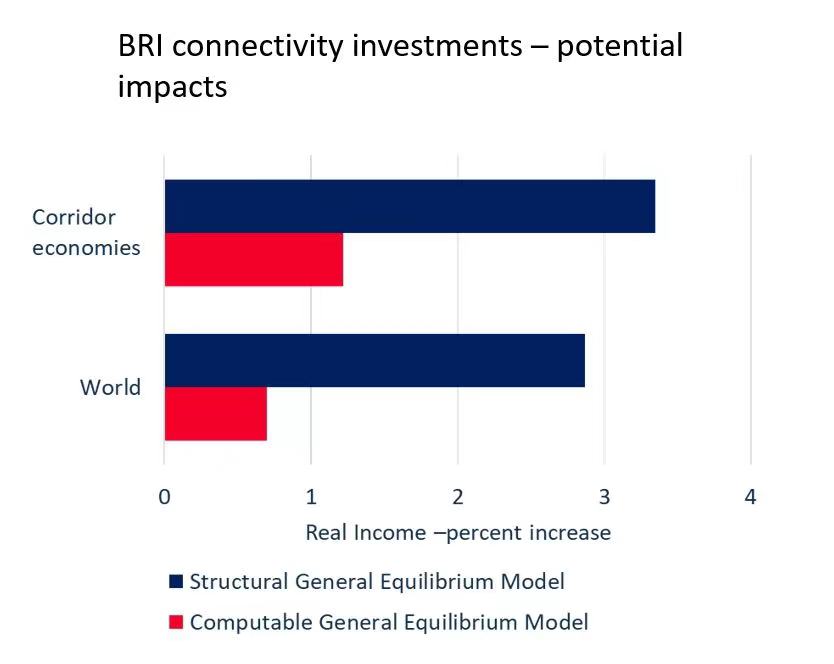

So by 2030, China's domestic consumption market would catch up quite a bit with the size of the market in the United States. And that would open-up opportunities for other developing countries. So rather than just giving up its role as a low skill manufacturing producer of export to other countries, I think China should also think about its own role as a consumer of some of those goods from developing countries. And by becoming a larger and more important market, I think China would open and significantly enhance or increase the opportunities that it offers to developing countries, in addition to what it does in building connectivity and in investing in infrastructure. With that, let me stop and thank you again for the opportunity. Thank you so much.

Editor: Olivia LOU

Dr. Martin RAISER

The World Bank Country Director for China, Korea and Mongolia